Note: These assumptions are now outdated. Our current capital market assumptions and our white paper documenting their construction can always be found on our Capital Market Assumptions page.

Sellwood Consulting’s 2015 Capital Market Assumptions are now available. These 10-year forward looking assumptions of asset class return, risk, and correlation are the key input variables for our client asset allocation work, including mean-variance optimization, Monte Carlo analysis, and risk budgeting.

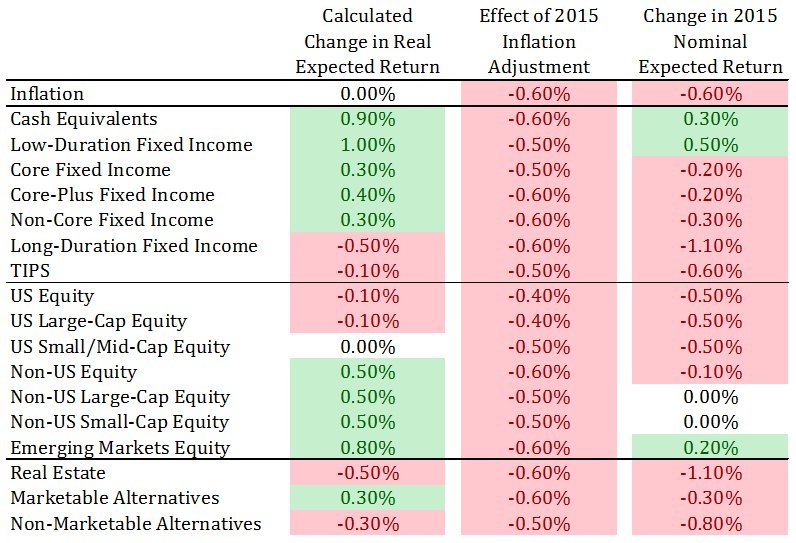

Declining inflation expectations over the course of 2014 were the primary driver of our changes to last year’s assumption set. During 2014, forward 10-year inflation expectations declined from 2.24% to 1.68% per year, a reduction of 0.56%. Given that our assumptions methodology first calculates a real return expectation and then layers onto it a current inflation expectation, most return assumptions declined by approximately the amount of decline in expected inflation.

The following chart depicts Sellwood’s 2015 arithmetic return assumptions, relative to those we created for 2014. The first column represents our calculated return changes, assuming no change in future inflation relative to last year. The middle column represents the effect of the inflation assumption’s change on the return assumption. The final column, at right, combines these two effects to depict our 2015 total change in nominal arithmetic return assumptions.

A rise in real yields at the short end of the US Treasury curve increased our return expectations for cash equivalents and low-duration fixed income (providing an example of the beneficial effects of rising rates). For longer maturities, declining real rates produced lower expected returns.

Our forecast for US equities, in real terms, is roughly unchanged. Extraordinary profit growth by US companies, over 2014, nearly offset the negative effects of higher stock market valuations over the year. Internationally, valuations declined, creating higher expected returns, especially in emerging markets.

More broadly, our assumptions continue to imply a prospective low-return environment for financial assets relative to historical averages. Further evidence of this environment has recently been highlighted by several credible industry researchers. Our assumptions are consistent with this analysis. Please also see our post, Realism in Forecasting, which explains our comfort with having forecasts outside the range of many of our peers.

Though we have made incremental enhancements to our methods for gauging the future value of assets, we have maintained our focus on the primary, reliable drivers of risk and return. Our assumptions are anchored in the empirical facts presented by long-term capital markets rather than speculative observations on recent market conditions. We avoid unnecessary complexity, preferring instead to rely upon transparent strategies that work reliably. Our analysis is comprehensive, but not complicated, because we are convinced that the most robust solutions have no hidden constraints and few moving parts. These same principles – pragmatic research and simplicity in execution – guide all of our work for clients.

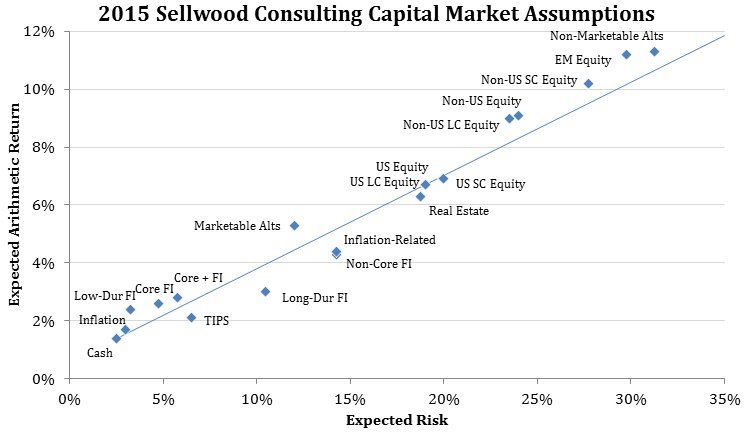

Presented in annual arithmetic average terms, our 2015 assumptions are depicted in the following chart:

Sellwood Consulting updates its capital markets assumptions on an annual basis. Our 2015 assumptions reflect information as of December 31, 2014, unless otherwise noted. Our assumptions are forward-looking in nature and reflect a ten-year investment horizon.

We have comprehensively documented our methodology and process for creating these capital markets assumptions in our updated 2015 Capital Market Assumptions white paper.

2015 Capital Market Assumptions by Sellwood Consulting LLC is licensed under a Creative Commons Attribution-NoDerivatives 4.0 International License.

2015 Capital Market Assumptions by Sellwood Consulting LLC is licensed under a Creative Commons Attribution-NoDerivatives 4.0 International License.