Note: These assumptions are now outdated. Our current capital market assumptions and our white paper documenting their construction can always be found on our Capital Market Assumptions page.

[insert_php]

$d1 = new DateTime(‘2013-02-28’);

$d1->add(new DateInterval(‘P1Y’));

$d2 = new DateTime();

if ($d2 > $d1)

echo “Note: These assumptions are now outdated. Our current capital market assumptions and our white paper documenting their construction can always be found on our Capital Market Assumptions page.

“;

[/insert_php]

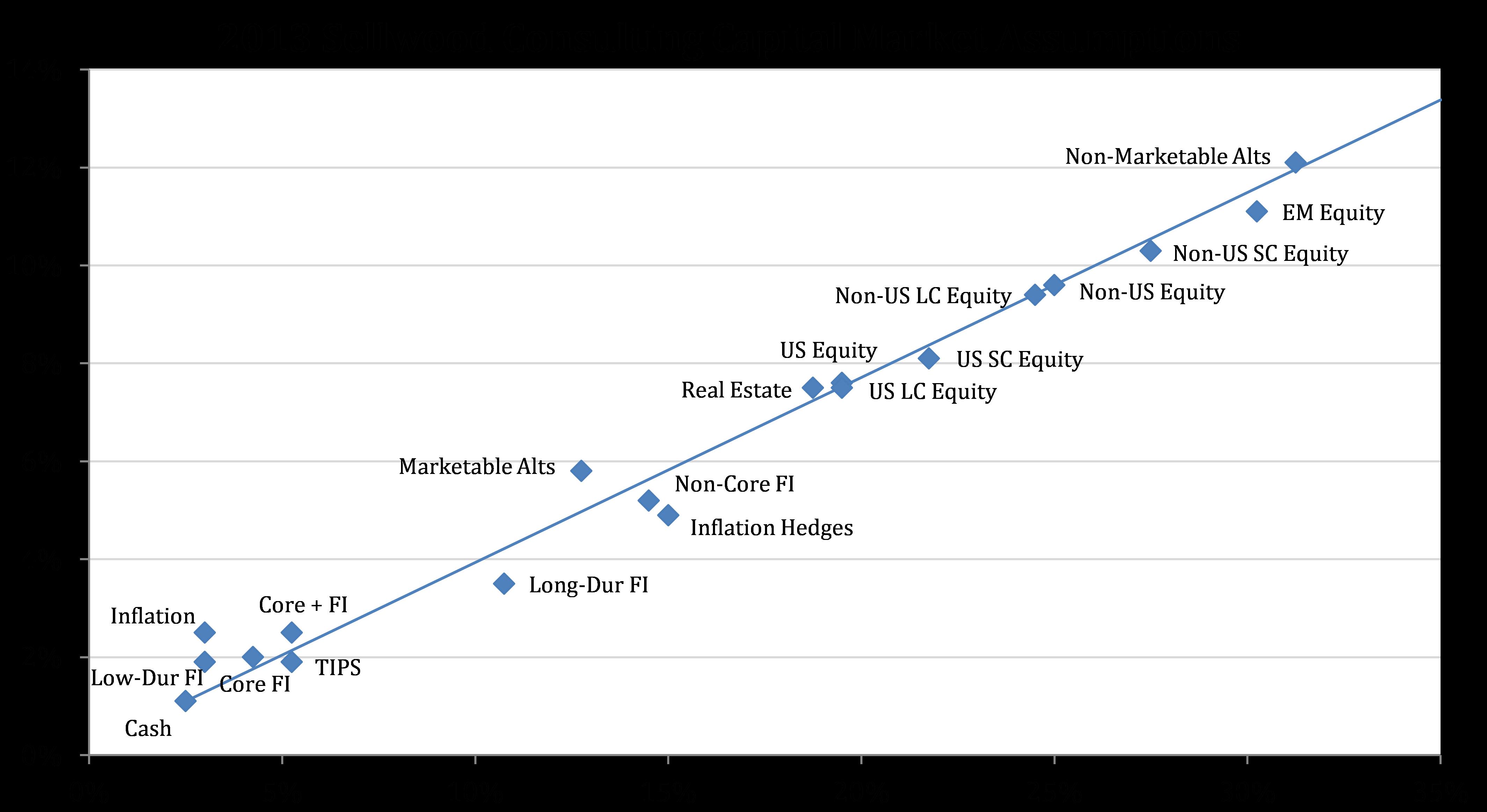

Presenting Sellwood Consulting’s 2013 Capital Market Assumptions.

Our forward-looking assumptions are the primary input for our asset allocation work for clients, being the input variables for mean-variance optimization, monte carlo analysis, and risk budgeting.

Sellwood Consulting updates its capital markets assumptions on an annual basis. Our 2013 assumptions reflect information as of December 31, 2012, unless otherwise noted. Our assumptions are forward-looking in nature and reflect a ten-year investment horizon.

[insert_php]

$d1 = new DateTime(‘2013-02-28’);

$d1->add(new DateInterval(‘P1Y’));

$d2 = new DateTime();

if ($d2 < $d1) echo

“This report documents our process for creating these capital markets assumptions, and we provide detailed methodology for each. You may download a PDF of the whitepaper.

“;

[/insert_php]

Our assumptions imply a prospective relative low-return environment for financial assets, given low current yields for equities and bonds. Further evidence of this environment has recently been highlighted by several credible industry researchers. Our assumptions are consistent with this analysis. Please also see our post, Realism in Forecasting, which explains our comfort with having forecasts outside the range of our peers.

Several over-arching principles inform all of our analysis regarding forward-looking capital market assumptions:

- We believe that forward-looking capital market assumptions are an important, but far from the only important, input for properly constructing portfolios. Great care should be taken not to rely only on mean-variance analysis when constructing portfolios. Generally speaking, an analysis that relies only on mean-variance analysis will over-allocate to assets with insignificantly superior risk/return estimates, and assets that are less liquid or less frequently priced.

- Our assumptions utilize a build-up approach based on the current values of the individual drivers of expected return that are unique to each asset class.

- For asset classes where the market provides a current view of forward-looking returns, our assumptions heavily weight the market view.

- Where possible, all of our assumptions incorporate current valuations. We assume reversion toward a long-term valuation mean over the prospective ten-year period. Where we have identified a current valuation and its long-term mean, our estimates consider a 50% reversion from the current valuation level to its long-term mean over the prospective ten-year period.

- Our assumptions are presented in nominal terms. Where we have used historical returns in our input analysis, we have always transformed them to real, after-inflation, returns, so as to strip out historical inflation. At the end of the build-up process, where appropriate, we add the market’s current measure of forward-looking inflation back to the assumptions to create nominal forward-looking return assumptions.

- Our base calculations are of and for compound returns. After calculating a compound return and a risk assumption, we combine the two mathematically to calculate an arithmetic expected return, which is a necessary input for mean-variance analysis.

- Our assumptions are passive in nature and assume no active management.

- Our approach to modeling the expected risk of each asset category is multi-faceted. First, we examine the historical standard deviation of the returns for a proxy index for the asset category (both the full history and most recent 10 years). Next, we examine the historical worst-case annual return experience (or in the case of asset categories that are not priced to market, the maximum two-year peak-to-trough experience) for the asset class. If necessary, we adjust our risk estimates to ensure that the actual worst-case experience had at least a 2% probability of occurring (once every 50 years) under our return and risk assumed distribution parameters. Finally, for asset classes where our confidence in the data available for examination is limited, we qualitatively adjust our risk assumption to reflect this uncertainty.

- Our correlation coefficient assumptions are mostly derived from history, with an emphasis on the recent past. We seek a proxy for each asset category we have modeled with as long a history as possible, and then calculate our correlation assumptions using a simple average of the following, for each pair of asset categories: Longest-term correlation; 10-year correlation; 5-year correlation; 3-year correlation. This approach purposefully overweights the recent past, while acknowledging the long-term past. It is also a more conservative measure for correlation benefit to a portfolio, because recent correlations have been higher than they have been historically.

- We round our assumptions to the nearest 10 basis points, in the case of arithmetic return, and nearest 25 basis points, in the case of risk.

2013 Capital Market Assumptions by Sellwood Consulting LLC is licensed under a Creative Commons Attribution-NoDerivs 3.0 Unported License.

2013 Capital Market Assumptions by Sellwood Consulting LLC is licensed under a Creative Commons Attribution-NoDerivs 3.0 Unported License.